Peer-to-peer (P2P) lending has rapidly emerged as a viable alternative financing model, providing direct access to loans without the involvement of traditional financial institutions such as banks. One of the notable players in this space is LenDenClub, India’s leading P2P lending platform. LenDenClub has been a pioneer in democratizing credit, especially in a country like India, where access to formal credit is limited for a large portion of the population.

Overview of LenDenClub

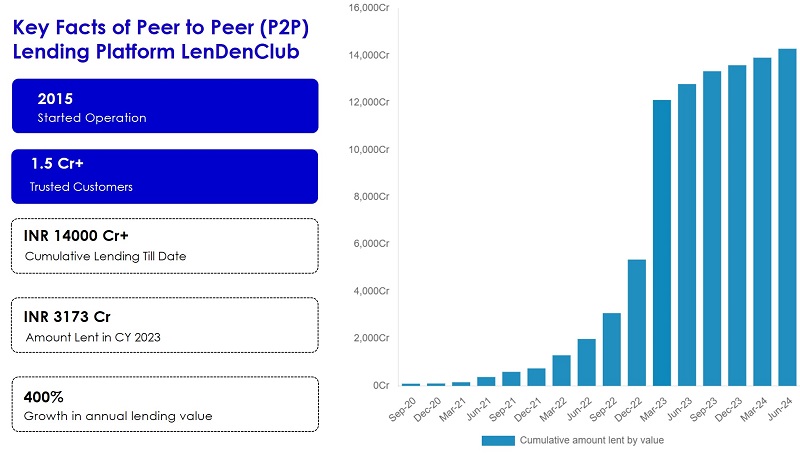

Founded in 2015, LenDenClub is a digital marketplace that connects borrowers looking for loans with lenders (or investors) seeking higher returns on their investments. As a regulated P2P lending platform under the guidelines of the Reserve Bank of India (RBI), LenDenClub operates with transparency and security, offering personal loans to borrowers and investment opportunities to lenders.

Key Features of LenDenClub:

- Loan Amounts: Typically ranging from INR 250.

- Loan Tenure: Short-term loans with a tenure of up to 36 months.

- Interest Rates: Interest rates depend on the borrower’s creditworthiness and range from 10% to 30%.

- Technology-Driven: LenDenClub uses advanced algorithms to assess borrower credit risk and match them with suitable lenders.

Core Value Propositions of LenDenClub

The core values of LenDenClub is to focus customer convenience and no/low fee lending facilities thorough a secure platform.

- Fully Digital Process: LenDenClub is a digital-first platform. There is no manual or physical interventions needed to start lending.

- Fund Diversification: The lending amount in the platform is hyper-diversified to as low as INR 1 among numerous loans to minimize risk.

- No Withdrawal Fee: There is no charge for the withdrawal of your funds. You can get your funds in your bank a/c within 24 hrs of placing a request post maturity.

- Zero Opening Fee: Opening an account on the platform costs you nothing. Open your P2P lending account at zero cost in less than a few minutes.

How LenDenClub’s P2P Lending Model Works

LenDenClub follows a simple, yet robust, P2P lending model where individuals or small businesses can borrow directly from individual lenders.

- Borrower Application: Borrowers register on the LenDenClub platform and submit personal details, loan requirements, and financial information.

- Credit Assessment: LenDenClub evaluates the borrower’s creditworthiness using various parameters, including credit score, income, repayment history, and other data points.

- Loan Listing: Once approved, the loan request is listed on the platform with all the necessary details for potential lenders to review.

- Lender Selection: Lenders (individuals or institutional investors) can choose the loans they wish to fund based on the borrower’s profile, interest rate, and risk category. Multiple lenders can contribute to a single loan, diversifying the risk.

- Loan Disbursement: Once the loan is fully funded, the money is disbursed to the borrower. LenDenClub handles all the documentation and formalities.

- Repayment: Borrowers make monthly repayments (principal and interest) to the lenders through the LenDenClub platform. The platform facilitates the collection and distribution of funds.

Benefits of LenDenClub’s P2P Lending Model

1. For Borrowers

- Access to Credit: LenDenClub is a lifeline for borrowers who may struggle to get loans from traditional banks due to lack of collateral, insufficient credit history, or being part of the informal economy. The platform offers unsecured personal loans without the need for collateral.

- Competitive Interest Rates: While the interest rates vary based on the borrower’s risk profile, LenDenClub often offers competitive rates, especially for those with a good credit score.

- Quick Loan Approval: LenDenClub’s streamlined, technology-driven process ensures that loans are approved and disbursed faster than traditional bank loans, often within a few days.

- Flexibility: Borrowers have the flexibility to choose loan tenures and amounts that suit their needs, without the rigid terms of traditional financial institutions.

2. For Lenders (Investors)

- Higher Returns: Compared to traditional investment options like fixed deposits or savings accounts, P2P lending through LenDenClub offers higher returns, ranging from 10% to 30%, depending on the risk profile of the borrower.

- Portfolio Diversification: Lenders can diversify their investments by lending small amounts to multiple borrowers, reducing the risk of significant losses due to defaults.

- Transparency: LenDenClub provides detailed borrower profiles and credit assessments, giving lenders control over the loans they wish to fund.

- Low Investment Threshold: Lenders can start investing with as little as INR 500, making P2P lending accessible to a wide range of investors.

Role of LenDenClub in Promoting Financial Inclusion

India has a large segment of the population that is underserved by traditional financial institutions. Many small businesses and individuals in rural or semi-urban areas do not have access to formal credit due to their lack of collateral or insufficient credit history. LenDenClub plays a crucial role in promoting financial inclusion by providing credit to these underserved individuals.

1. Bridging the Credit Gap

LenDenClub helps bridge the credit gap for small businesses, entrepreneurs, and low-income individuals by offering them access to loans without the need for complex documentation or collateral. This is particularly beneficial for:

- First-time borrowers who may not have established credit histories.

- Small businesses in need of short-term working capital to meet operational expenses.

- Consumers who need quick access to personal loans for emergencies, medical expenses, or other short-term financial needs.

2. Boosting Economic Activity

By facilitating loans for small businesses, LenDenClub supports the growth of micro and small enterprises (MSMEs), which are the backbone of India’s economy. Access to credit allows these businesses to expand, hire more workers, and contribute to overall economic development.

3. Empowering Individual Borrowers

LenDenClub’s simplified loan process empowers individual borrowers by giving them access to capital that they can use to address personal financial needs, such as education, healthcare, or home improvement. This, in turn, enhances their economic independence.

Risks and Challenges in LenDenClub’s P2P Lending Model

While LenDenClub provides significant benefits for both borrowers and lenders, it also faces some challenges inherent in the P2P lending space.

1. Risk of Default

The biggest risk for lenders is borrower default. Although LenDenClub conducts thorough credit assessments, lending is inherently risky, especially with unsecured loans. If a borrower defaults, lenders may not recover their full investment.

- Mitigation: LenDenClub allows lenders to diversify by spreading their investments across multiple loans, reducing the impact of a single default.

2. Regulatory Challenges

Although LenDenClub operates under RBI guidelines, P2P lending is still a relatively new and evolving sector in India. Changing regulations or tighter oversight could impact the platform’s operations.

3. Lack of Liquidity

Unlike traditional investments in stocks or mutual funds, P2P lending involves illiquid investments. Lenders must wait for borrowers to repay the loan over the agreed term, which can take months or years.

The Future of LenDenClub and P2P Lending in India

The future of LenDenClub looks promising as P2P lending continues to gain traction in India, driven by rising demand for alternative financing models and the digitization of financial services. LenDenClub’s ability to innovate, scale, and adapt to regulatory changes will determine its long-term success.

1. Expansion of Services

LenDenClub has the potential to expand its offerings by introducing more diverse financial products, such as business loans, microloans, and education loans, catering to a broader audience of borrowers.

2. Integration of Technology

The adoption of AI and machine learning for credit scoring, fraud detection, and borrower-lender matching will enhance the platform’s efficiency and accuracy, reducing the risk of defaults and improving the customer experience.

3. Increasing Financial Literacy

As more Indians become aware of alternative finance options like P2P lending, LenDenClub can play a key role in educating consumers about the benefits and risks of these platforms. This will help bring more lenders and borrowers into the formal financial system.

LenDenClub has emerged as a pioneering platform in India’s peer-to-peer lending landscape, offering a win-win scenario for both borrowers seeking access to quick, unsecured credit and lenders looking for higher returns on their investments. By leveraging technology, transparency, and customer-centric services, LenDenClub has positioned itself as a key player in driving financial inclusion and alternative finance in India. As the platform continues to grow and innovate, it will play an increasingly important role in the future of lending and investing in the country.